BNEF’s reputation as progressive on EV adoption projections is in question after its latest Electric Vehicle Outlook report trims its previous projections of sales across the coming decade down 10%, and assumes annual growth rates will quickly drop to 23–24% from the current rate of 56%. The main bottleneck BNEF sees is battery manufacturing capacity. By the firm’s in-house estimates, battery manufacturing capacity grows only enough to supply 10 million EVs annually by 2025. Leading battery forecasters, Benchmark Minerals, see future battery capacity much higher than this. Let’s breakdown the BNEF report and provide an alternative outlook.

BNEF treads a tricky line between analyzing and advocating for “New Energy” technologies whilst not upsetting the incumbent legacy players (and the orbiting array of financial analysts) that make up a significant proportion of its clients.

To its credit, BNEF has had the honesty to admit that many of its past projections in the new energy space are consistently and “embarrassingly” behind the curve, always “getting it wrong on the downside” as they put it:

(2432) BNEF’s New Energy Outlook 2018 – YouTube

Unsurprisingly then, BNEF’s track record in “EV Outlook” reports has consistently underestimated the true growth rates. BNEF’s 2017 EV Outlook predicted 1.02 million passenger EV sales for the year, a growth of 46.7% from 2016’s 695,000 sales. Eventual 2017 sales — by BNEF’s own subsequent reckoning — were 1.091 million, a growth of 57%.

Undeterred, in April 2018, BNEF’s Outlook projected EV sales would grow from 2017’s 1.091 million to 1.59 million in 2018, an increase of 46%. BNEF actually switched its methodology after this (previously counting just passenger vehicles, now counting all LDVs — light duty vehicles) so the analysts didn’t hand in their homework for their 2018 projections. Several other reliable data sources, including those of EV Volumes, confirm total LDV sales of 2.1 million in 2018, up 72% from 1.22 million in 2017. Assuming passenger vehicle sales grew at least as much (largely thanks to the Tesla Model 3), BNEF’s prediction of 46% was another significant miss.

We’ll look more closely at BNEF latest forward projections, and the reasoning behind them, below.

Why Does BNEF Have Such an “Embarrassing” Track Record?

As I’ve mentioned before, the forcing function for highly paid industry analysts and consultants is that clients are unlikely to blame the ones who paint bland, cautious, conservative, and ultimately unmemorable projections, which in fact turn out to underestimate rates of change several years down the line.

Clients are much more likely to blame consultants that predict a rapidly changing industry (requiring large investments to stay abreast of) in the event that those changes don’t materialize (and those investments are wasted). The short story is that forecasters very often simply get paid to provide “expertise” that bolsters and reconfirms the perspectives that industry stalwarts have already adopted. The suits and ties lend credence to the game.

In the broader predictions business, BNEF says that it sees its peers as the oil companies, cartels, and energy agencies (wedded to a fossil fuel worldview). BNEF lists Exxon, BP, OPEC, the IEA, and the EIA as its peers. Most of these organizations obviously have good reasons not to be progressive in predicting the growth of EVs. For anyone not familiar with the IEA, we’ve documented its determinedly laggard attitude to cleantech several times over the years, as we have for years with similarly horrid EIA projections. With peers like these, it’s an easy posture for BNEF to stand a step apart from the pack and then be able claim that its modest (and always behind-the-curve) forecasts are “the most progressive.”

BNEF’s 2019 EV Outlook

This year’s BNEF EV Outlook projects sales in 2025 will be 10 million (down from 2018’s projection of 11 million). Projected 2030 figures are down to 28 million from 2018’s 30 million. The main reason for these lackluster numbers is BNEF’s modeling of battery manufacturing capacity out to 2025 and 2030. It sees the 10 million limit in 2025 not due to any lack of demand, but constrained by its projected 1 TWh global battery cell manufacturing limit in 2025.

The report assumes two thirds of this 1 TWh annual capacity in 2025 will go to passenger EVs, which will each require an average of 66 kWh (gross) battery capacity. The result is only enough supply for 10 million vehicles in 2025.

There’s no scope for future growth of battery manufacturing capacity in BNEF’s modeling — the forecast for capacity in 2025 (6 years from now) appears to be locked down. But it’s worth noting that BNEF does not claim leading expertise on battery manufacturing pipelines.

Benchmark Mineral Intelligence is the leading specialist in this area. Here at CleanTechnica, we regularly report on Benchmark’s research updates. Here’s what the company’s founder and CEO, Simon Moores, says about their mission:

“At Benchmark Mineral Intelligence, all we specialise in is the lithium ion battery supply chain. Our Lithium Ion Battery Megafactory Assessment is a month by month, plant by plant analysis of global capacity build out.

“We spend the entire month collecting and analysing data points to add or take away new capacity from our database. We also map this out by year, format and cathode chemistry to calculate the raw material impact. It’s the world’s most robust system for the industry and it’s why the supply chain uses our data to plan expansion timelines.” (Simon Moores, Benchmark)

Simon Moores recently hosted the Benchmark Minerals Summit 2019 in Washington, DC. Benchmark’s track history of work with the US government has already had a positive impact on US policy. Senator Lisa Murkowski made the following statement:

“I recently spoke at the Benchmark Minerals Summit on our foreign mineral dependence. The significance of foreign oil dependence is widely understood, but our foreign mineral dependence is equally – if not more – serious.

“Last year we imported at least 50 percent of 48 minerals, including 100 percent of 18 of them. That should worry everyone, particularly because it is happening at the same time that demand, for everything from graphite and lithium to cobalt and nickel, is about to skyrocket.

“I have introduced the American Mineral Security Act, a bipartisan bill that takes a comprehensive approach to rebuilding our domestic mineral supply chain. Unless we take significant steps, we’re at risk of ceding major economic drivers to other countries.” (Senator Lisa Murkowski)

I recently spoke at the Benchmark Minerals Summit on our foreign mineral dependence. The significance of foreign oil dependence is widely understood, but our foreign mineral dependence is equally – if not more – serious. pic.twitter.com/D9cy5HaB39

— Sen. Lisa Murkowski (@lisamurkowski) May 3, 2019

My point is that BNEF’s lowball assumptions about battery manufacturing capacity are not the only perspective, and they are not the leaders in this area of forecasting. Benchmark’s Simon Moores has a different view of the future:

“[As of May 2019] We have battery capacity surpassing 1TWh by 2022/2023. In 2025 we have this at 1.35TWh… This isn’t a forecast however. This is an assessment of what is in the announced pipeline. More is coming, especially in North America, so our forecast for capacity would be 20% higher at least.” (Simon Moores, Benchmark)

This tilts Benchmark’s current 2025 expectations towards 1.62 TWh and potentially higher (and still with room to grow between now and 2025). Although, details of announced plans on the US side will take time to materialise and get counted in Benchmark’s official figures.

I have previously argued that China’s vehicle ownership culture is significantly different from that of Europe and the US, with vehicle-kilometers-travelled each year being much lower, and cars being mostly used for urban area commuting, not long-distance inter-city travel. The latter is handled by high-speed rail and flights. With increasing efficiency, the average battery size of EVs in the Chinese market (mostly pure BEVs, but some PHEVs) will likely be around 50 kWh by 2025, not 66 kWh. Plug-in hybrids (PHEVs) usually have 15–20 kWh batteries, at most. China will comprise around half of global EV sales by 2025, so this differential is significant. Remember that vehicle designs optimised for EV powertrains can have decent interior space even in a compact external footprint. Compact cars and CUVs with moderate battery sizes are likely to dominate the Chinese, other East Asian, and European markets.

Combined with Benchmark’s battery capacity forecast, and still allowing for a third of battery supply to go to other use cases, this gives scope for 21.4 million EVs of average 50 kWh each in 2025, over twice BNEF’s EV unit figure. Even if 66 kWh is the average pack size, that’s still 16.2 million EVs in 2025, 62% above BNEF’s numbers. All this is assuming the 2025 battery manufacturing pipeline only grows modestly in the coming years.

BNEF’s Numbers Compared to Growth in Demand

By putting the battery supply forecast as the main influence on future EV sales, BNEF ‘s report is arguably putting the cart before the horse. Ultimately, investment in battery capacity, mineral supply, and EV production capacity will be a function of demand and not the other way around. On the basic consumer appetite for EVs, BNEF’s report recognizes the current reality, saying, “Over 2 million electric vehicles were sold in 2018, up from just a few thousand in 2010, and there is no sign of slowing down.”

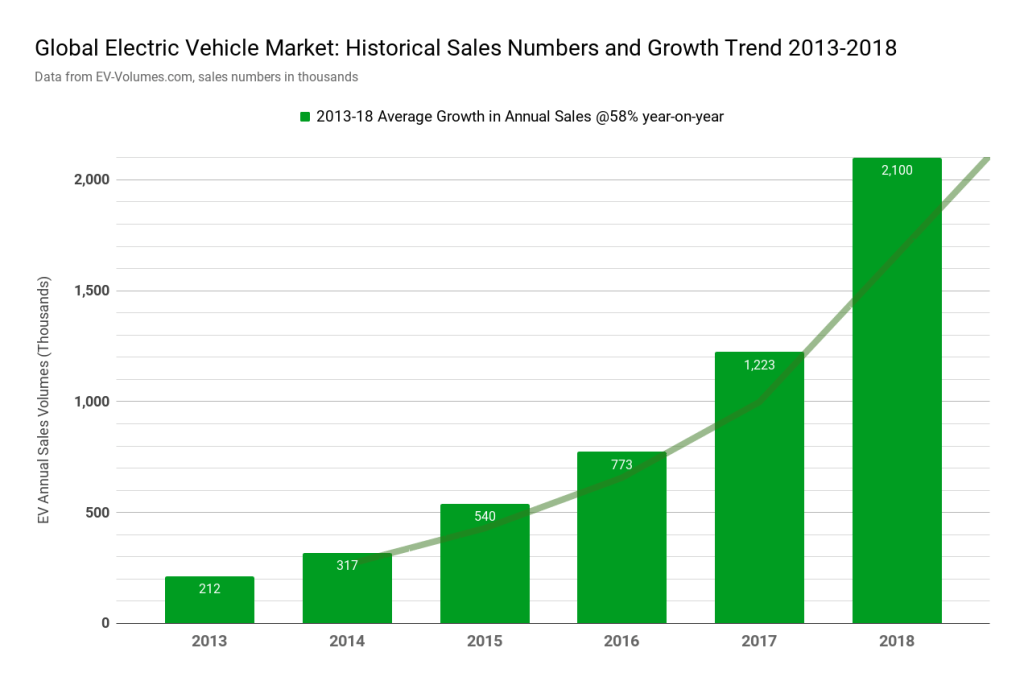

As we saw above, the past 5 years have seen global EV sales growing at 58% per year on average, with the past 2 years actually outperforming the 5-year average. BNEF undoubtedly knows that 2019 Q1 has already seen YoY growth of ~57%, right in line with the 5-year average.

For BNEF’s forecasted 10 million sales in 2025 to hold, near-term annual growth rates would have to immediately drop to 26% from their current ~57%. Looking further out, BNEF predicts 28 million in sales in 2030, which corresponds to a 24.5% average annual growth rate between 2025 and 2030. Is this realistic?

Bear in mind that, precisely in this period — the mid-2020s — BNEF itself “expect[s] price parity between EVs and internal combustion engine vehicles.” Given the total cost of ownership of EVs is already superior to fossil vehicles today, in many cases, the obvious question is — why would anyone still want to buy the latter, once upfront price parity is also unambiguously surpassed?

Understanding the growth in demand for new technology may be best understood by looking at historical trends. The history of technology adoption shows that, once market penetration of a new technology passes a foothold of around 2.5% to 5%, it then quickly takes off. US household adoption of automobiles moved from 2.5% to 50% in around 12 years. Color TV made the same shift in around 8-10 years, as did microwave ovens, cell phones, and the internet.

For EVs, this 2.5% to 50% transition has already happened in Norway, taking around 7 years. Iceland is on track, with the move from 2.5% to >25% (expected this year) taking 5 years. Its 2.5% to 10% move took 3 years. Sweden is passing 10% this year, 4 years after passing 2.5%. China passed 2.5% in 2017–2018 and looks set to pass 10% in late 2019 or 2020 (around 2.5 years). Q1 2019 saw 7.5% EV market share in China.

Although these markets are the leaders, and other markets are lower down on the adoption curve, the latter are following the same general pattern. As EVs are quickly getting ever more affordable and capable, there’s every reason to expect that the adoption curve in these other markets will see growth at least as fast.

For the global market as a whole, EVs are already at around 2.3% market share in Q1 2019 (some 500,000 sales), up from 1.3% in Q1 2018, and will hit 3% later this year. The historical record discussed above suggests it may only be another 2.5 to 4 years or so before 10% global market share is reached. That’s likely 2022 to 2023 for 8 million to 10 million global annual EV sales. This also fits with Benchmark Minerals’ battery capacity assessments, as we saw earlier.

This high demand growth perspective is corroborated by growing EV reservation queues in many markets. The demand for EVs is there and it is growing fast. This points to a related dynamic that Maarten recently analyzed in his Osborn Effect article. People are increasingly willing to defer purchases of legacy fossil vehicles and wait for an EV. This contributes to further increasing the market share of EVs, as fossil vehicle sales drop in absolute terms. The BNEF EV Outlook doesn’t discuss or acknowledge these kinds of market dynamics.

Other BNEF Blind Spots

BNEF believes that a portion of urban dwellers who may not have access to a plug at home or work will not be able to participate in EV ownership any time soon. The report states “one of the most interesting questions over the next 10–20 years will be how to address buyers who [have no access to charging at home or work].” This is certainly not a limitation in Oslo, the world’s leading city for per capita EV sales.

In Oslo, “62 per cent of all residents in the capital live in a block of flats,” according to the most recent national census data. EVs’ share of auto sales in Oslo passed 57% in 2018. Evidently, a high proportion of apartment dwellers has not been a barrier to high EV market penetration in Norway’s capital.

China is focussing strongly on ensuring that electrical outlets (mains voltage, 220 volts) are accessible in apartment building parking areas, and other countries are also rolling out building codes to encourage this. A standard mains 220–240 volt outlet (80% of the world’s population) is sufficient for all but the most extreme commuting patterns, giving at least 20 to 25+ kWh of energy overnight. For efficient compact or midsize EVs, this equates to more than 80–100 miles, 130–160 km, of daily range — which is approximately double even the USA’s average per driver, or approximately quadruple the European average.

On a related note, the BNEF report suggests that the added cost of a dedicated home charger and installation must be built into the cost equation of EV ownership when considering cost parity with fossil vehicles. Although a dedicated home charger gives EV owners extra flexibility, we’ve just seen that they are not strictly necessary in the 220–240 volt regions that most people live in. Even in the 110 volt US, overnight charging on a standard dryer outlet can provide decent service to typical commuters. Is a dedicated home charger desirable? Certainly. But BNEF’s claim that a dedicated home charger is a necessary added cost to EV ownership is not strictly accurate for most regions.

Meanwhile, even without home or street-side charging for apartment dwellers, there are other practical options. Urban DC fast chargers, capable of giving typical EV drivers a week’s worth of commuting range over the course of a 20–30 minute grocery shop or coffee stop, will be widespread by the mid-2020s. Tesla already has Urban Superchargers in major US and Canadian cities. Most combustion vehicles need dedicated visits to gasoline stations around once per week, which can’t overlap with other activities. It’s not clear that a pattern of parking-lot-charging outside of a store should be considered any more burdensome for itinerant EV owners than gas-station visits are, especially with the transactionless “plug and charge” (and even wireless) protocols that are now coming to market.

Finally, BNEF has some outlier predictions that seem to defy all logic. One example is its forecast that — having reached 9.5 million annual sales in 2030 (a little under 50% market share) — China’s EV sales will grow by just 4.25% annually between 2030 and 2040 (reaching 14.6 million sales, around 70% market share in 2040). Why the predicted lethargic China growth rate in the 2030s? At this time, by BNEF’s own reckoning, EVs will already be far less expensive to buy and own than fossil vehicles. No explanation is given for this seemingly outlandish claim.

Summary

BNEF’s past EV Outlooks have all proven far too conservative in light of realities on the ground. Its 2019 downshift seems not to be primarily motivated by concerns over demand growth, but instead a pessimistic view of available battery supply in 2025 and thereafter. Other, better qualified, battery forecasters document planned battery supply pipelines significantly higher than BNEF’s gloomy numbers.

I’ve previously set out an argument that China’s EV market share can readily reach 50% by 2025. Some European markets are on target to be well ahead of this, and others will not be far behind. Canada, East Asian regions, and other markets are also already on the move. China and Europe comprise 50% of auto sales. Rather that BNEF’s downbeat — and battery constrained — forecast of 10 million sales in 2025, there’s every reason to expect at least 21.4 million sales (around 20% to 25% global market share) by that time. The best research shows that planned battery production capacity will be in place to enable these numbers.

What do you think? Is BNEF still being too conservative? Is the analysis of the numbers I’ve given here too bullish (on not bullish enough)? Please share your thoughts, reasoning, and comments.

Leave a comment