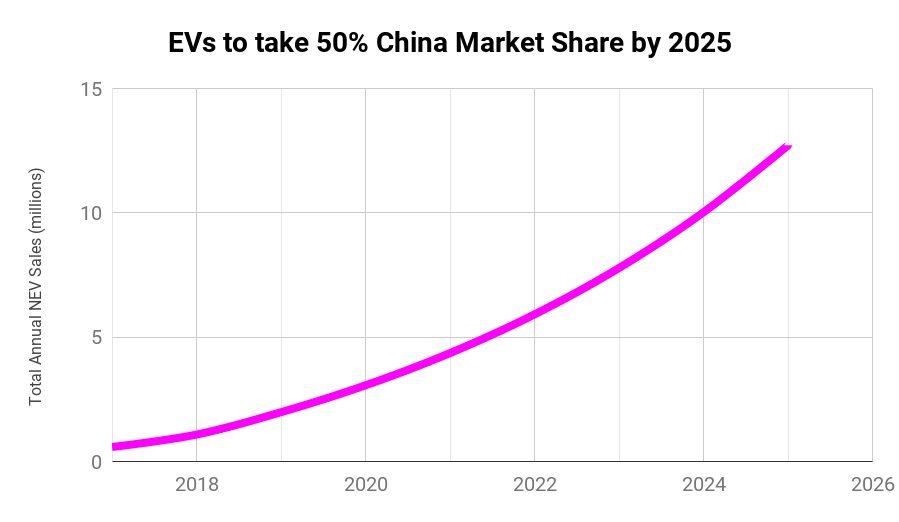

China is charging full speed ahead into electric vehicles, on track to sell over 2 million EVs this year, up from 1.1 million in 2018. The rapid growth has been driven partly by policy, but increasingly by consumer demand. In part two of this three-part series (check out part one if you missed it), we’re going to look at the demand side of the EV transition in China. Why are Chinese consumers queuing up for EVs?

Queuing out the Door for EVs

Did you know that the petite BYD Yuan (below) had a waiting list of 40,000 customers at last count? More folks are joining the queue, even as 10,000 units per month are being produced (and ramping up). NEVs in China are in very high demand from consumers. Even the premium-end Nio ES8 had 17,000 reservation deposits ($750) before production began. This is Nio’s first vehicle, highlighting the palpable demand for EVs. And of course the big hitter for EV queues is Tesla and its Model 3, with an unknown number (several tens of thousands) of reservation holders in China. The Model 3 has just started arriving in customers’ hands in the country.

Given that the market share of EVs is already significantly higher than in other large markets, we have to ask — why are Chinese consumers so keen on EVs, compared to average European or US car buyers?

NEVs already have a cachet over traditional vehicles for China’s wealthier buyers, and an ever-growing portion of the middle class is opting for consumer choices perceived as environmentally friendly. This is also the case in limited parts of the US (e.g., California) and some parts of Europe, but on average is more pronounced in the Chinese middle class, partly due to the critical problem of combustion engine pollution in many Chinese cities. More generally, the car-buying portion of the population is closely tuned in to technology trends and forward-looking in consumer behaviour (witness the rise of mobile payments in China, for example).

NEVs already have a cachet over traditional vehicles for China’s wealthier buyers, and an ever-growing portion of the middle class is opting for consumer choices perceived as environmentally friendly. This is also the case in limited parts of the US (e.g., California) and some parts of Europe, but on average is more pronounced in the Chinese middle class, partly due to the critical problem of combustion engine pollution in many Chinese cities. More generally, the car-buying portion of the population is closely tuned in to technology trends and forward-looking in consumer behaviour (witness the rise of mobile payments in China, for example).

With EVs representing a widely recognised growing technology trend, the direction of consumer preference towards EVs and away from fossil vehicles — to which there is zero positive cultural attachment — is indisputable. Most car buyers in China are the first person in their family to ever own a car, and have no lingering childhood memories of riding in their mum’s Ford Pinto, their uncle’s Mustang, or their neighbour’s pickup truck. A generation ago, only a tiny proportion of the population owned a car of any kind. There is limited attachment to cars in general, and no nostalgia for fossil powertrains, nor inertia holding people back from accepting the inherently better technology of EVs. And everyone living in Chinese cities (including most car buyers) is fully aware — inescapably aware — of the pollution problems inherent to combustion vehicles.

EV Range Already Sufficient for Most Chinese Owners

Is the current (and evolving) state of the technology already past the point of being good enough for Chinese car buyers? Whilst US and European buyers want long-range EVs because they expect to occasionally make long journeys in their cars, this use case is very rare (almost non-existent) for Chinese car owners. Most are city dwelling middle class folks who use their cars for commuting in and around the city. As a side note — the auto market in general also has much lower penetration potential in China than in Europe or the US, because whilst autos are mainly bought to move around very dense cities, it’s actually much faster to move around Chinese cities via the extensive and modern metro rail networks, which are highly developed:

“There is uncertainty about the long-term motorization track that China could take. Sustainable transport and pollution policies of its cities, energy security policies, the drive to invest in public transportation infrastructure, new connected technologies, and the high-density living of its urban population all point to a decline in the desire to own a vehicle even as real income levels rise. This diverges from the trend seen in the West, where car ownership has increased in step with higher income levels.”(Nigel Griffiths, chief economist, IHS Automotive)

Similarly to other East Asian societies, journeys between cities are not usually made by road at all. Instead, these are also made by high-speed, high-frequency, and affordable rail networks, or by plane for very long distance. There is essentially no road-trip culture in China (nor other societies in the region), and the median vehicle kilometres travelled (VKT) per year in China will likely stabilize close to that of Japan. Japan has the lowest VKT of any OECD society, less than 40% of that in the US. Prof Minggao Ouyang and colleagues researched driving profiles of car owners in and around Beijing and found that – even on public holidays – less than 1% of auto trips made are over 120 km (75 miles). That’s well within the range capability of almost all EVs already.

Concerns about range and fast charging infrastructure, that are so topical in Europe and the US, have little resonance with Chinese vehicle owners. Even so, China has 75% of the world’s EV chargers and much focus is being put on improving this supporting infrastructure even further. The GB/T charging standard’s merger with CHAdeMO will also bring V2G capabilities to China’s EV fleet, which can potentially help China’s push towards more renewable power generation.

EV Value Proposition Relative to Fossil Vehicles

The passenger experience in EVs is inherently superior in ways that are appreciated by Chinese consumers. EVs have more passenger space than a fossil vehicle of the same exterior size segment, due to removing much of the space given over to combustion engine and transmission. EVs are smooth, refined, vibration free, and inherently luxurious (quiet, responsive, powerful, etc.), all qualities appreciated by middle-class Chinese consumers.

This sense of greater space, comfort, and luxury gives EVs much greater value than an otherwise “equivalent” fossil vehicle. The interior space and comfort in EVs is often equivalent to that in fossil vehicles in the segment size above. This in turn means that the price / value proposition of EVs is already superior to fossil vehicles in many cases, and almost always already so in TCO comparison.

Adopting for a moment a positive cultural stereotype, based in part on my 10 years living in the culture as an anthropologist, many members of the Chinese middle class are often fiscally wise, and are thus relatively quick to recognise the TCO advantages of EVs even if the sticker price might have a premium over fossil vehicles that might (externally) appear to be similar. Of course, as EV production ramps up, the sticker price gap with fossil vehicles will quickly close, likely in the next 2 or 3 years in most segments of the Chinese market. The premium segment is already there in many cases. When Tesla’s Shanghai Gigafactory starts producing the Model 3 later this year, it will have local pricing far below that of the imported BMW 3 Series and Audi A4.

Consumer Adoption Accelerators for EV Market Share in China

Past experience has shown that, once EVs have a market share of around 10%, as has happened in Norway and Iceland, the general awareness of EVs as the superior technology and inevitable future sets in. This then tends to have a compounding negative effect on willingness to pay hard-earned money for “new” fossil vehicles that lock purchasers into an outdated and inferior technology with higher running costs. Even if EVs are not immediately available in the desired quantities, consumers will prefer to wait until they can buy an EV, and thus reservation queues and waiting lists develop (as is already happening in China). In saturated auto markets like Norway, this waiting period just means keeping hold of your existing vehicle for a bit longer. In the China market, the same pattern applies to existing vehicle owners. For the large portion of first-time buyers — who have anyway been anticipating and perhaps saving up for auto ownership for several years — it’s not hard to understand that they would prefer to wait a few more months, or even a year, for an EV, instead of buying an old-technology fossil vehicle.

The point at which EVs penetrate a society enough that many folks make up their mind that their next (or first) auto purchase will be an EV, not a fossil, is obviously a death knell for the older technology. In anecdotal terms, general awareness of EVs’ technological superiorityoccurs when someone you know personally, whether from work or social connections, has bought an EV and is – as usually happens – telling everyone within earshot how much better the experience is, and that they will never own another fossil vehicle, and wish they’d made the switch earlier.

This awareness-to-action turning point arrives a bit earlier than 10% market share in China. Unlike in Europe or the US, many larger cities in China have a high proportion of EV taxis and buses, so experience of riding in EVs and awareness of their superior technological, financial qualities, and experiential qualities is already very high. In other words, the “big turning point” is already happening this year and next in China, even before reaching 10% of market share.

Finally, as hinted above, with huge production volume and batteries being locally produced (more on this in part 3), China’s EVs will be price-competitive with fossil vehicles at least as quickly as in any other market. For most categories, this will happen well in advance of 2025. Once the sticker price is lower, on top of the running costs being lower and the driver and passenger experience being much better, there will be little motivation for anyone to purchase a new vehicle that is anything other than an EV, and sales of fossil vehicles will further plummet. This dynamic will strongly boost EV market share relative to fossil vehicles. It’s easy to win market share when your competitor is declining in absolute sales volume.

Autonomy & Ride Hailing

Several auto OEMs offer different and more premium rear-seat options for the China market. Why? Because a significant proportion of affluent middle-class Chinese car owners prefer to be a passenger and have someone else drive for them, even in the car that they themselves own. This preference underlines the huge difference in car culture between China and the US (and Europe). It also suggests the reason why a recent survey found that 89% of folks in China feel ready to jump into an autonomous vehicle, whereas the figures are much lower in Germany (52%) and the US (50%). There are a large number of homegrown autonomy efforts in China looking to capitalise on this sentiment, and the government is encouraging it.

There’s a high possibility that at least some autonomous EV services (“robotaxis“) will start to become available for popular routes in the larger Chinese cities by 2025, if not earlier. Once this happens, private vehicle sales will take a further hit, and all autonomous vehicles will be electric, for economic reasons. The purchase of a fossil vehicle will seem an even more outdated decision. Whatever production volume of EVs that has been achieved by the time autonomy arrives will thus represent an even larger % share of the new sales market relative to fossil vehicles.

Finally, even without vehicle autonomy, China has huge growth in ride-hailing services like Didi, just as the US has Uber and Lyft. Younger generations are gravitating to these, which will further cool the demand for private vehicle ownership. This potential decline in overall volume of auto sales again allows a given manufacturing production volume of EVs to take more market share. It’s worth noting also that high-mileage working vehicles are more economical in EV format than in fossil format (due to fuel and maintenance savings).

Finally, there’s the dynamic of the consumer’s sense of future regulations (whether or not these regulations actually come into effect). Everyone knows that fossil vehicles have malignant side effects, but that mobility is generally a good thing. Thus, the negatives have only been accepted (and pushed to improve via emission controls, etc.) to the extent there has not been a viable alternative technology for auto-mobility. With the rise of EVs, this changes. Every part of the previous Faustian compromise can be consigned to the history books.

There’s therefore the palpable sense that city, regional, and national government regulations (see part 1 for fuller discussion of these) may be emboldened to further restrict fossil vehicles. This dynamic only increases the consumer’s perspective that fossil vehicles are an outdated technology on the wrong side of history, further accelerating their decline in sales and boosting market share of EVs.

Consumers in China are Looking to the Future — and Seeing EVs

Let’s summarise: Chinese middle class consumers are tech-forwards, and all vehicle ownership is relatively new. There are no positive cultural attachments or memories from childhood about fossil vehicles, they are widely understood to be polluting. Compared to Europe and the US, living density and alternative mobility options and preferences are very different in China. The city-based duty cycle of most private autos means that even modest-range EVs are already attractive and cost-effective for the vast majority of auto buyers. EVs also have inherent characteristics which are valued by middle class consumers, especially interior space and refinement.

Greater awareness of EVs amongst the urban middle-class car buyers, and greater awareness of their overall value advantage, is also powering the change. Autonomy, mobility services, and avoiding being on the wrong side of history are factors that may further speed the transition.

Given that the policy push for EVs in China is strong, and the consumer demand is also strong, the only remaining question is — how fast can China ramp up the production of EVs, and the batteries that power them?

Look out for part 3 of this report.

Leave a comment