China is charging full speed ahead into electric vehicles, on track to sell over 2 million electric vehicles this year, from 1.1 million in 2018. The rapid growth has been driven partly by policy, but increasingly by consumer demand. In the 3rd and final part of this series (check out part one and part two, if you missed them), we look at the ramp up in EV production and battery supply. Will production capacity be able to keep pace with the rapid growth in EV demand?

Recent Growth Trend and How Fast Forward?

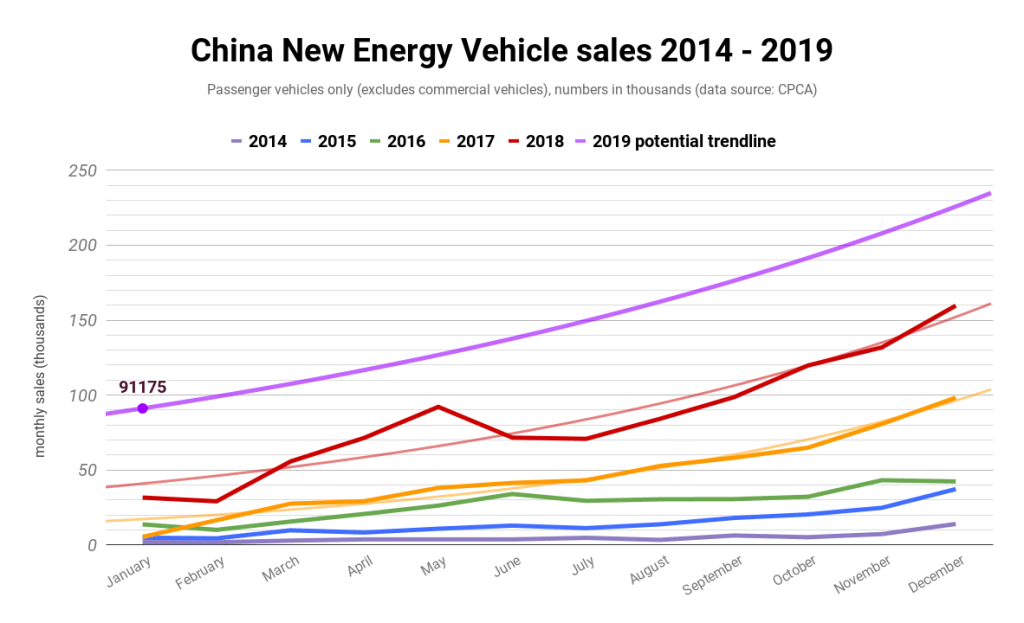

We saw in part one that China’s January 2019 figures put EVs on track for 2 million sales in the country this year. That’s an 82% year-on-year growth in volume over 2018 (1.1 million), depending on how you tally up the exact numbers (passenger cars only, or all light-duty vehicles, or all vehicles including buses and heavy-duty vehicles). With 2 million sales, the EV market share of total light-duty vehicle sales will increase from 4.1% in 2018 to 7.5% in 2019.

We know China’s manufacturing efforts can ramp fast, since the growth in traditional auto production and sales scaled from 2.4 million in 2001 to 17 million in 2010.

A simple extension of EVs’ 82% current annual growth trend, against a stable background of 28 million annual light-duty vehicle sales (the 2017–2018 volume), might suggest EVs reaching 50% market share sometime in late 2022. Taken at face value, the sequence would be 2019’s 2 million => 3.6 million => 6.6 million => 12.1 million in 2022, likely overcoming 50% of auto sales in the final month or two of that year. But high initial growth rates are more easily achieved from a low base. Even if the consumer demand for EVs is there (see part two of this series), bringing online 5.5 million units of extra EV production capacity (across all parts of the supply chain) from 2021 to 2022 would be a monumental task.

More conservatively, the manufacturing compound growth rate will likely slow from its current 82%. Slow by how much?

It’s not so hard to conceive that the volume of “new production capacity added or converted” each year will continue to rise. Why converted? EV production is not all that different from traditional auto production, apart from the requirement for batteries, electric motors, and power electronics (especially inverters). China already has a production capacity for 28 million autos per year. For many Chinese auto OEMs, completely new buildout of EV production lines may not in fact be necessary. It will instead often be a matter of converting combustion vehicle production lines or facilities over to EV production.

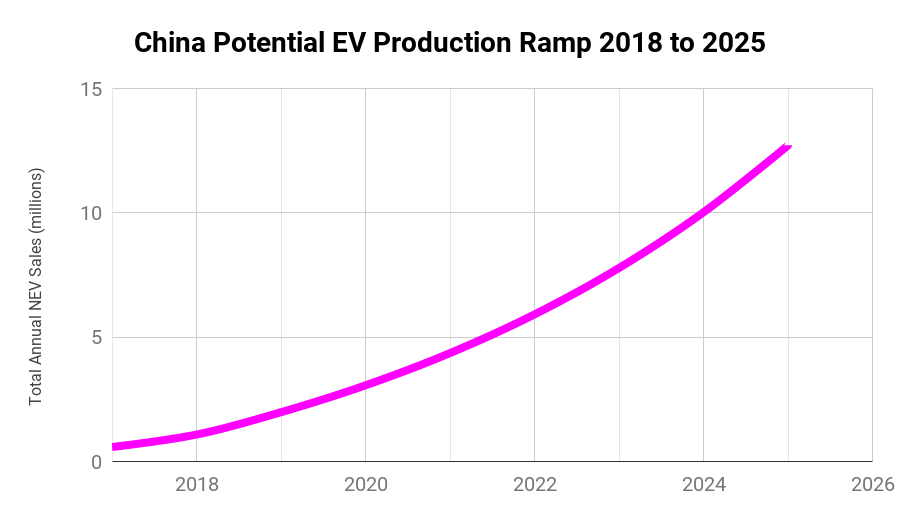

Whatever the mix of conversion or all-new capacity, EV production capacity at a growing rate would require repeating, with a modest increase each year, the effort and resources dedicated to the task. Since 900,000 units of “new production capacity” looks set to be brought online and into operation in 2019, it may be reasonable to assume the possibility of a 20% annual growth in new-or-converted capacity. This would give us an additional 1.08 million units of capacity in 2020, 1.3 million in 2021, and so on. Here’s the sequence:

The provisional conclusion here is that — if the demand is there — with a big push but not unreasonable assumptions, the actual vehicle production capacity side of things will probably not be a bottleneck. We can see that the overall compound growth rate falls off from 82% towards 50%, 40%, then 30%. Nevertheless, this would still result in 12.7 million total EVs produced in 2025, with the final months of the year trending higher and reaching approximately 50% market share. This of course assumes maintaining 2017–2018 size of total auto market (28 million), when in fact the overall size may be significantly smaller because of the wait-for-an-EV effect outlined in part two, and other dynamics we covered there. Here’s the graph of the resulting total EV production:

But how about the battery supply to power all these new EVs? It’s one thing to be able to have the manufacturing capacity to build EVs in theory, but surely ramping up battery supply is the more likely bottleneck?

China Battery Factory Capacity on Track for 16 Million EVs by 2025

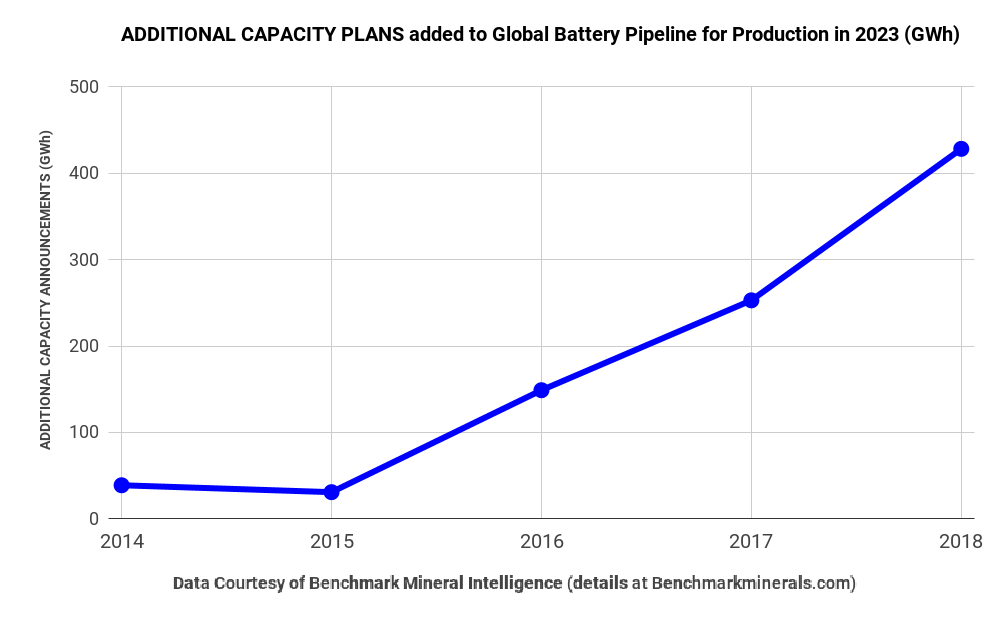

In 2014, Tesla announced a plan to bring online a huge new capacity of 35 GWh per year of lithium-ion battery supply. This was of course the famous Gigafactory 1 in Nevada. We covered this story extensively at the time.

Back then, it seemed like an ambitious plan, to double the world’s then lithium-ion battery production capacity in just one huge project. But then in the following year, 2015, additional plans were announced from other quarters, which amounted to another 31 GWh capacity brought online by the early 2020s.

From there, guess what? In 2016, yet more planned new additions were announced, adding 149 GWh of extra capacity to the world’s total 2023 production capability. You can probably see a pattern emerging.

In 2017 — oh, just a further 253 GWh. And yes, of course, in 2018 yet more again – another 428 GWh! This pattern will continue in the next few years. Here’s the graph of new-and-additional announcements by year (this is not the cumulative total — that’s the subsequent graph):

So, when we add all of this up, where does it get us to? What’s the total global capacity now in the pipeline to be ready for production by 2023? 922 GWh. And 1549 GWh by 2028 (chart below). The data are robust, from Benchmark Mineral Intelligence, which has kindly given me access to some of its subscriptions, which track all of the world’s lithium-ion battery mineral mining and processing developments, and pricing, as well as planned battery capacity ramps. I’m planning on doing a profile of Benchmark soon, so stay tuned for that. Here’s its January 2019 chart:

Notice that around 66% of the world’s battery production capacity — in any given year — will be in China. If we statistically derive the pipeline capacity 2025, this puts us just under 800 GWh annual battery capacity planned for production in China by that date.

This is announced plans as of early 2019, and assumes that there are no further announcements of new planned capacity added between now and 2025. There will be plenty of new announcements, because as well as EVs (not just in China, but globally), there will be huge worldwide demand for battery stationary storage, both at utility scale and behind the meter at homes, business premises, factories, hospitals, public buildings, etc. There will also be increased demand from other modes of transport (mopeds, bikes, etc.) as well as for at least certain classes of ships, off-highway vehicles, drones, and ultimately for at least some planes (in the longer term). In short, 1549 GWh in 2028 is not nearly the end point of future global battery demand. It’s likely to be at least an order of magnitude or more. Thus we will see additional battery production capacity planning being announced over the coming years.

Translating Batteries into EVs

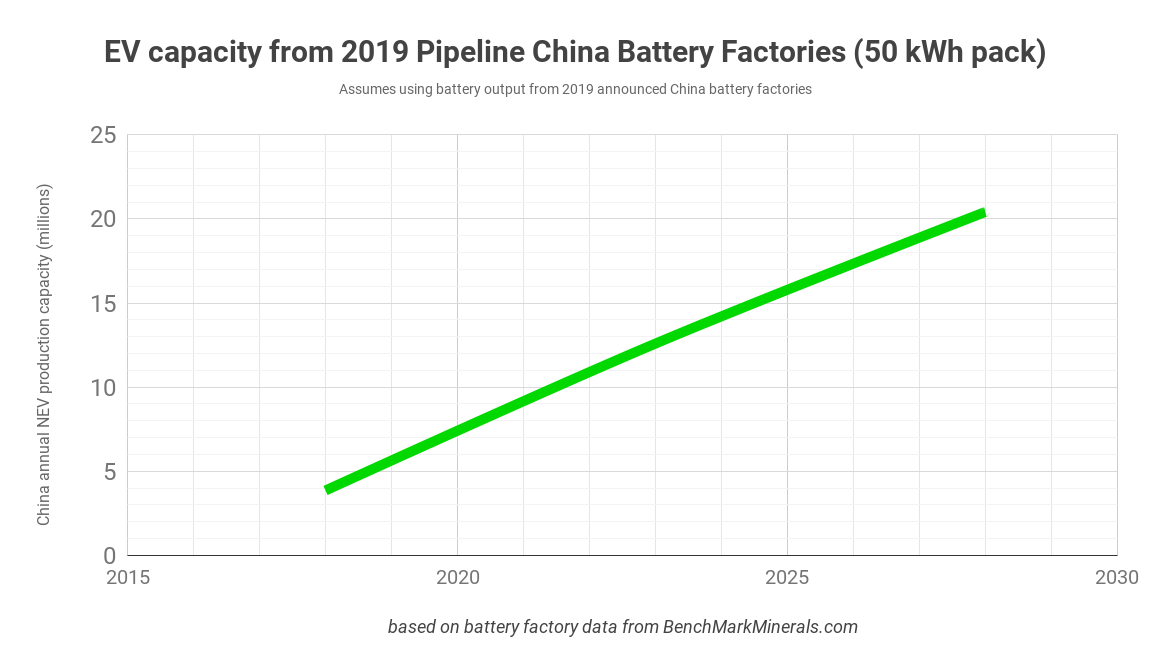

If, as of today, China is already planning to have 630 GWh of annual battery production capacity online by 2023, 800 GWh by 2025, and 1021 GWh by 2028, how much annual EV production capacity does that provide?

It of course depends on the average size of battery in each vehicle. At the moment, in the 2018 20-best-selling NEVs in China, the top 5 BEVs have an average battery size of 55 kWh, and the top 4 PHEVS (there are only 4 among the top 20 NEVs) have a 20 kWh average. The China BEV-to-PHEV ratio in 2018 was 4:1 in the top 20 best sellers. This means that, on the basis of the most popular vehicles, the average NEV in 2018 has a battery size of 48 kWh.

In part two of this series, I said that many Chinese consumers are already happy with the range of their NEVs. And we’ve seen that the new NEV credits policy is pushing for, and rewarding, greater efficiency of NEVs. Given the modest range requirements of the China market, I estimate that 50 kWh may settle to become close to a typical battery size, at least in 2025. It will certainly be enough battery for the vast majority of China’s auto buyers. On this basis, we can translate the planned battery production capacity in China into EV numbers:

China’s 800 GWh of annual capacity in 2025 allows for an EV production volume of 15.9 million units, which is well above 50% of new auto sales. It also easily accommodates the EV production ramp that we looked at above. Even if the average battery size increases to 60 kWh, the 800 GWh by 2025 still translates to 13.3 million EVs (and ~50% of market share). Let’s go further upstream in the supply chain to check out any other possible bottlenecks.

Lithium!

As Simon Moores, (founder of Benchmark Mineral Intelligence) said to me recently, given the rapidly growing demand for EVs, the most likely bottleneck may be for lithium raw materials from mined sources. Lithium is in fact a minor constituent by volume (or weight) in lithium-ion batteries, despite their name, but it is the technologically-key chemical constituent. It is also critical in the sense that the feedstock materials and ores required for battery chemicals (lithium carbonate and lithium hydroxide) traditionally only have relatively small mined quantities, relative to the quantities now increasingly in demand.

Nickel, aluminum, and manganese (along with graphite, below) are other key components, but are already mined (for other uses) in substantial quantities, so none are critical, though nickel will need to ramp up. Graphite is important but is not as critical as the lithium materials, in terms of relative supply quantity. Cobalt is fairly critical in supply (and troubled), but its ratio is being reduced in batteries, so it is not strategically as critical as the lithium sources.

China already has over 50% of the world’s lithium processing plants to produce battery grade lithium product. China also has supply contracts that command most of the lithium feedstock supply. The same is true of China’s relationship with cobalt. Graphite, the key anode material is mostly mined in China anyway. 100% of the processing of graphite into material suitable for battery anodes is also done in China. So there’s no great obstacle for China (other than scaling up processing facilities) in producing enough of the processed lithium chemicals to make batteries, so long as the feed-stock supply can be sourced in sufficient quantities.

On the lithium mining front, the game is in play, and miners know that the market for battery-grade lithium is very quickly ramping up. Australian mines currently supply over 50% of the lithium raw material for batteries. China’s own domestic mines contribute a little over 10%, but China has mining investments and tight supply agreements in Australia also. Albemarle, the world’s biggest lithium raw material producer, has just seen its share price jump by 6% and is currently expanding operations at its Australian lithium mines, as well as its operations in South America (Chile and Argentina combined supply another ~40% of global lithium raw material for batteries). Albemarle has just released its latest quarterly report stating that:

“Our growth will be driven by increased volume in our core lithium business. … We are not forecasting any significant macroeconomic headwinds and have not seen any decline in our customer demand forecasts.” (Albemarle)

There’s also room in the lithium mining and processing industries for more players, so expect to see frequent announcements of new lithium mining resources and lithium processing plants being brought online as well as expansion of existing projects in the months and years ahead. Mineral supplies will be a fast-moving area for the EV transition, and needs attention, investment, and effort to ramp up to meet the fast growing demand. However, there are no fundamental roadblocks here that will derail the speed of transition, so long as the communication lines are open and pricing signals and other market signals are all working well.

Conclusion — the Short March to 50% Market Share

China’s appetite for EVs is not slowing down, and looks set to grow by a further 82% this year and achieve 7.5% market share of 2019 auto sales. The market share will probably exceed 10% in December. Due to strong policy support (see part one) for clean transport and strong consumer demand (see part two), combined with cultural factors and other positive feedback effects, there is every likelihood that EVs will take 50% market share of autos in China by 2025.

China-based lithium-ion battery factories are already in the planning pipeline to produce enough capacity to meet the growing domestic demand for EVs, and capacity plans will continue to grow rapidly to accommodate demand from stationary storage applications and other use cases. There is little risk of battery production capacity overshoot by the mid 2020s, due to the multiple growing markets for battery energy storage. As of January 2019 there is enough planned battery production capacity in China to supply 16 million EVs by 2025.

Combustion vehicle sales in China fell from 2017 to 2018. They will fall off more sharply each year, crossing below 50% market share in 2025, and quickly diminishing to a small residual portion of road vehicle sales by 2030 (probably under 20%), likely dying out almost completely by the mid 2030s. The precipitous fall in the volume of combustion auto sales in the next few years, and possible overall auto market shrinkage (see part two) will make it easier for a given volume ramp of EVs to win relative market share on the approach to 50%.

We’ve covered quite a bit of ground in this three-part series (thanks for making it this far). If there’s anything that seems unexplained, please read all parts, preferably in sequence. If you have any thoughts, reflections, different angles, or suggestions for improvement, please do join in the comments.

Leave a comment